The market drove itself into the end of the second quarter (June 30, 2024) with the same group of usual suspects. Again. It hasn’t been the same since. July turned the page and it was a whole different tune, lyrics and rhythm. Small cap, Mid cap, and the whole silo of Value took to the stage and wowed everyone while those who have led for so, so long languished and saw their stock prices falter or simply fall. This was exacerbated as earnings season kicked off and the scrutiny began in a way we haven’t seen for some time. This scrutiny meant just beating revenue and earnings were not enough. If you typically beat expectations, you needed to do so with emphasis. You needed a strong outlook. All the important business lines needed to be firing on all cylinders. While this was occurring, less expensive stocks were being rewarded with inflows from the outflows coming from the stocks that were “priced to perfection”.

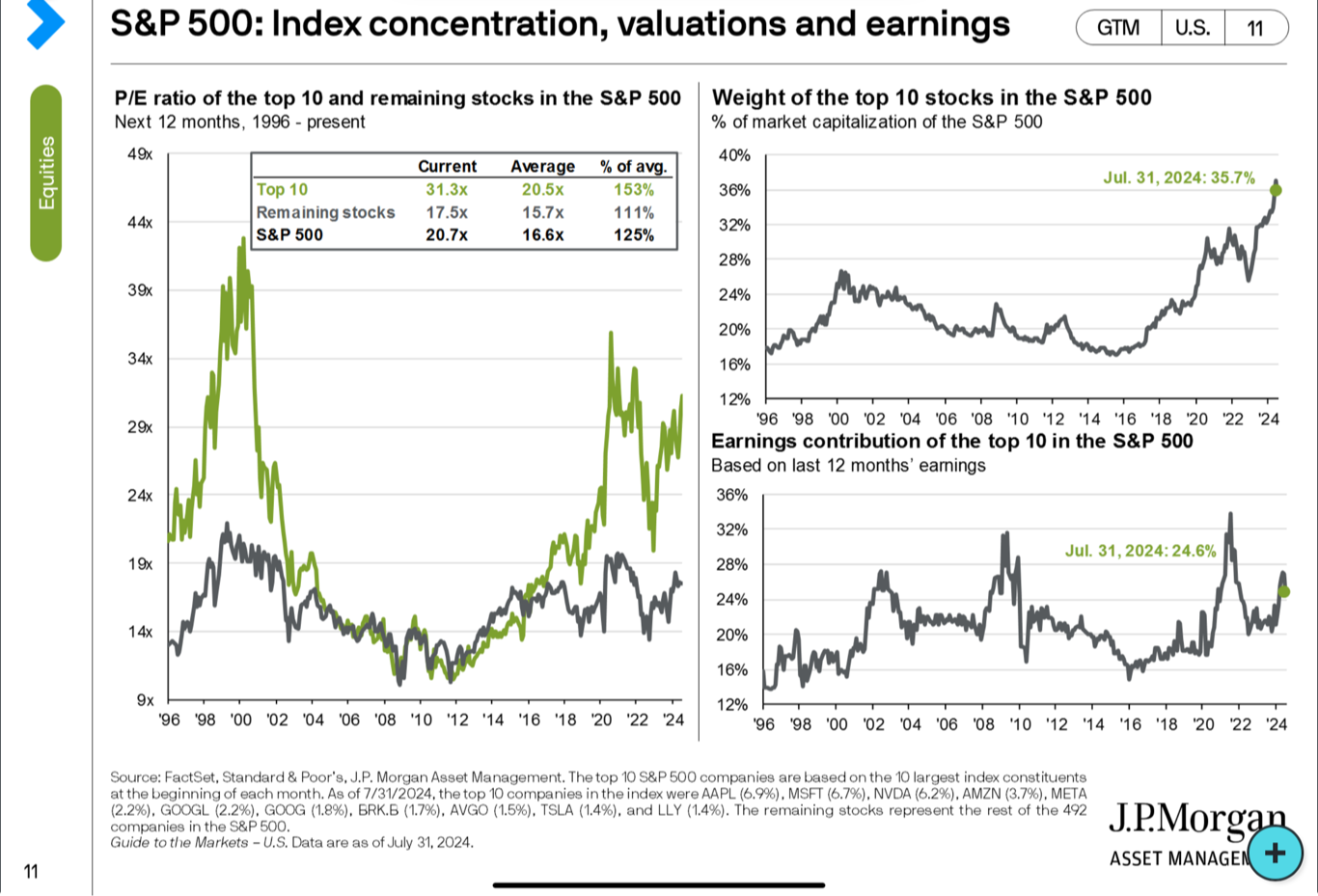

The investment world is a interest place of dichotomies and divergences, generalities and specifics. The “market” was considered expensive because the price to earnings was above historical norms. However, if one dissects the market a bit and considers how the S&P500 is constructed (by largest market capitalization to smallest), one might get a clearer picture that all is not expensive.

However, if one dissects the market a bit and considers how the S&P500 is constructed (by largest market capitalization to smallest), one might get a clearer picture that all is not expensive.

Another narrative was also simultaneously playing out; the “soft landing”. The narrative of this was The Fed has read the economy and employment and has taken all the appropriate actions to ease the economy and markets into a more normalized position post COVID stimulus. The financial world has oscillated to and from this story a couple times. In 2022, The Fed actions (late, albeit) were so strong many were calling for a recession (in fact, nearly all major economists). In 2023, when this didn’t occur and crow was summarily eaten by the dismal economists, the markets got extremely excited in late 3rd quarter when The Fed indicated the end of the rate hiking cycle and hinted via the “dot plots” of a future in which they may lower rates- not because things were bad, but because inflation, the economy and employment normalized. The three cuts insinuated were quickly conflated into six (6!!) by the market and a strong rally ensued fed by this imaginative number of rate cuts and the artificial intelligence craze. The Fed worked for several months to talk down the markets dream of six cuts. It slowly deflated it back to “maybe one or two” for the whole year of 2024 —if the economic numbers continued to prove out.

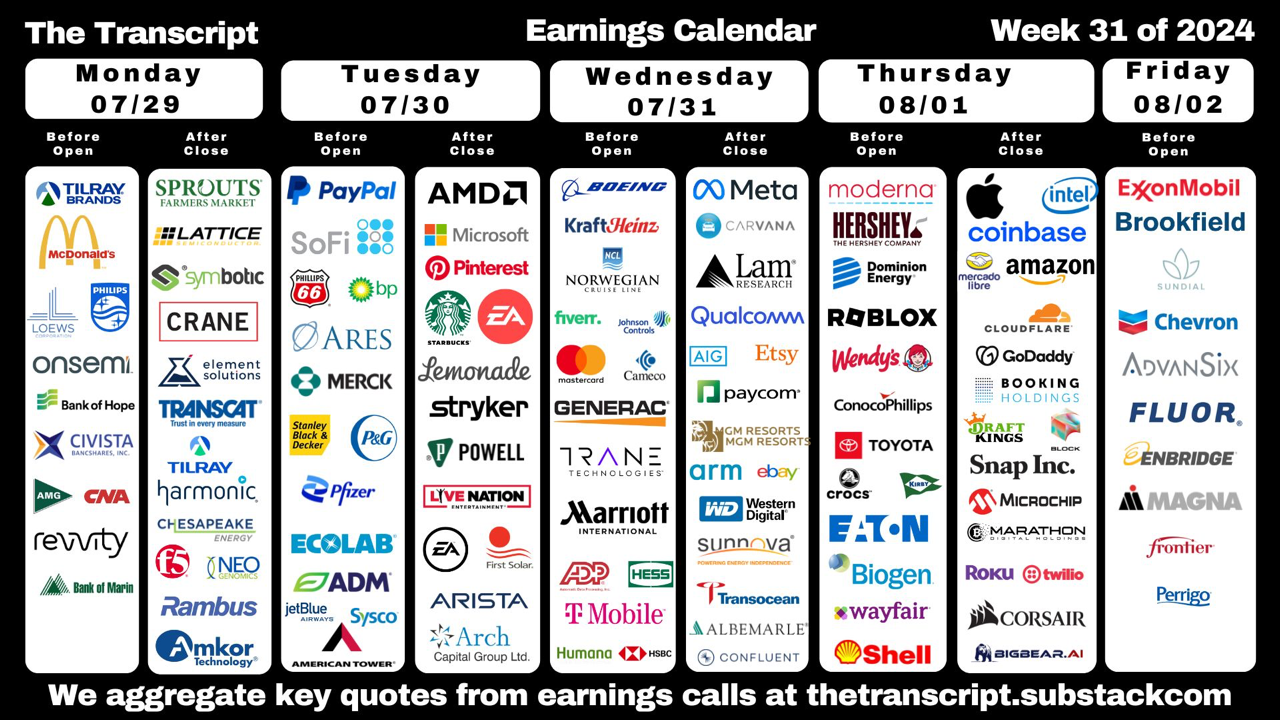

So here we are, August, with a July that seemed to have moved in way anticipating rate cuts in September and maybe December. Then last week happened. The week of July 29 thru August 2 was the highest percentage of S&P500 companies reporting. Also many of the largest, important companies were reporting. Its a week of companies that are a good representation of the economy.

Additionally, there was The Fed meeting. It was widely expected they would take no action, but it was widely expected Jay Powell’s press conference after would confirm that September was a “live” meeting, meaning they would probably cut the Fed Rate. Everything happened as planned. The market rallied strongly on Wednesday afternoon as the press conference continued.

A small irritating grain of sand, the ADP employment report on Wednesday came out. It was far weaker than expected. Under the “soft landing” narrative, bad news was good, so it was largely dismissed. However Friday was the BLS (Bureau of Labor Statistics) employment number and unemployment rate. It was much weaker than expected and unemployment rose. AND, the BLS revised down the June numbers and the May numbers. This combined with “not great” earnings reported on Thursday’s close (Intel removed their dividend and announce a layoff of 15% of their workforce), and the narrative quickly changed. Bad was bad and perhaps the “soft landing” was going to experience some turbulence and the flight attendants would need to buckle in with the passengers!

Over the last weekend, filings revealed that Berkshire Hathaway (Warren Buffett) reduced their position in Apple stock by over 50%. They had over a billion shares so that is a lot of reducing and did not instill confidence in Apple. They also reduced their Bank of America position. There is never any commentary on these moves until something official like a quarterly report of annual report, so the “why” is unanswered with ample speculation in the financial community.

Lastly, over the weekend Japans market opened in turmoil being down over 7% at one point, triggering their market’s circuit breakers. This is what the U.S. market woke to Monday morning.

There are events outside the markets and the economy that may be influencing actions too. There are worries the Israel/Hamas conflict may be in process of escalation. We as a country are experiencing an unusual presidential election cycle. An attempted assassination. A candidate stepping down. A presumed new candidate outside the norm of primaries.

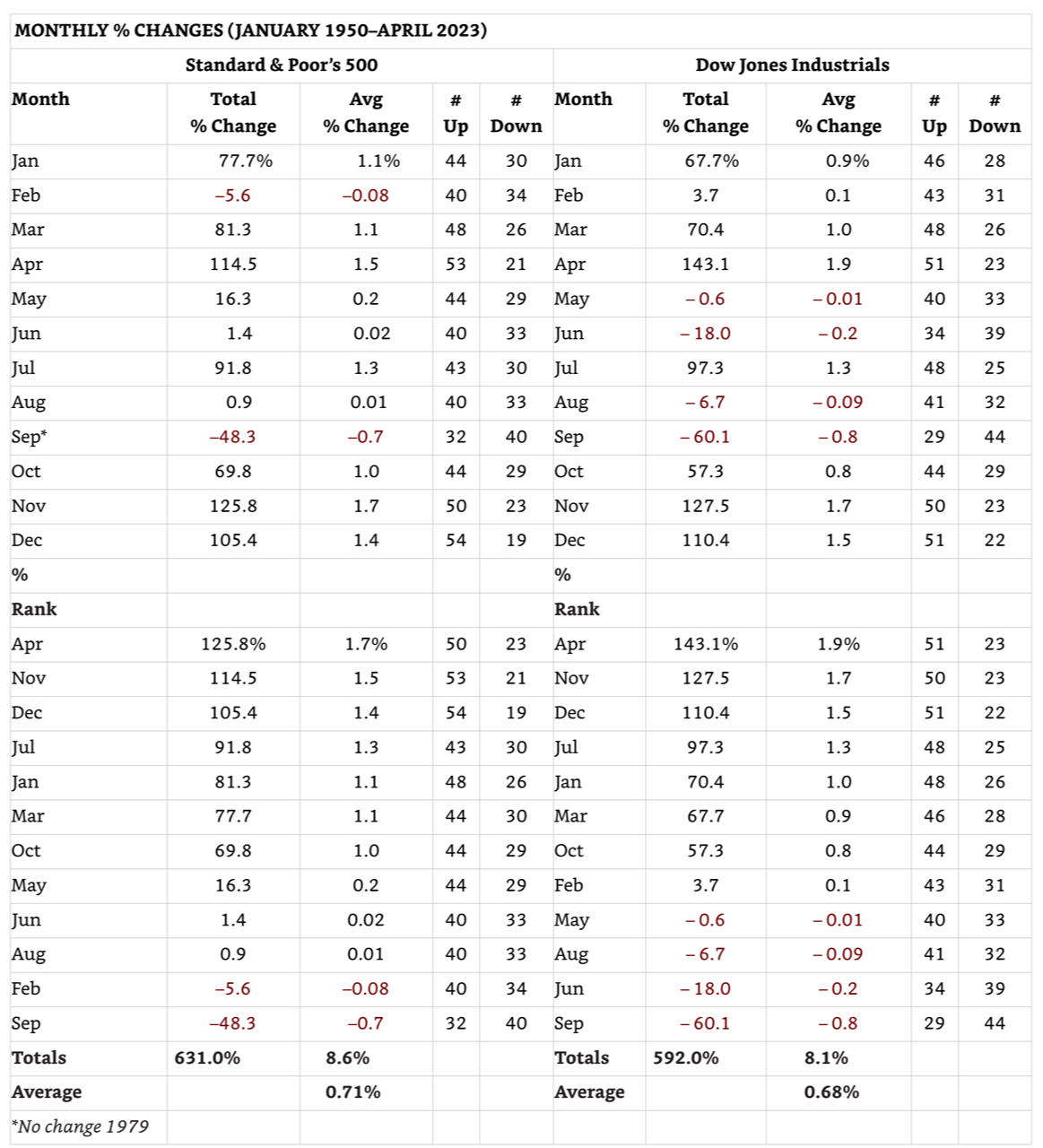

It is not at all clear that a recession is in the future. And it takes time for such a thing to occur when it does. I am operating on what information I have and is present, not what could or might be. The tone has changed dramatically. We are at the beginning of two historically weak months as can be seen in the table below from “The Stock Trader’s Almanac”. These are averages, so each year can differ. (e.g. April of 2024 was not good. Down nearly 5%)

Source: The Stock Traders Almanac: 2024

I expect continued volatility and softness. The bulk of critical earnings have past. The Fed has no meeting in August, but has a conference in Jackson Hole with the world’s Central Bankers and the like. Mechanically, The East Coast people take their last summer vacations which, believe it or not, cause a drop in volume and liquidity for the markets in their absence. There will be many economic data points along the way to The Fed’s September meeting, which is “live”. However, expectations are now very high the cut should be 0.5% which last Wednesday the expectations were only 0.25%. There is a risk of expectation/reality mismatch. We have a Democrat Convention in Chicago and all sorts of news flow surrounding the presidential election to muddy the waters too.

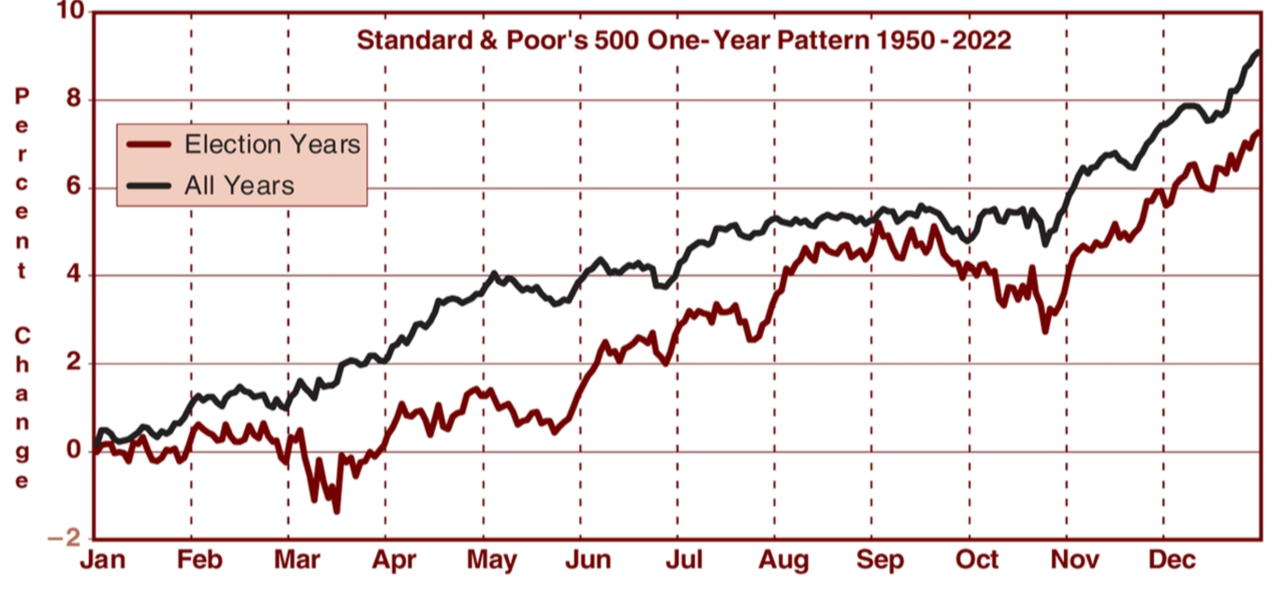

This is why on Friday and Monday I took action to sell some stocks and raise cash. The thesis for the positioning has changed. The technical charts and fundamentals on many of the stocks has changed. The market is at the start of a historically weak period. Bullish sentiment as of last Thursday was too high and while it has likely dropped in the two days that followed, we are early on and it is prudent to move through this period with a more prudent, cautious positioning. I will continue to take in all the economic and market data and make the best decisions I can. I am still operating under the thought we need to be repositioned in a more normal fashion just before the Presidential election because historically the market rallies strongly to the end of the year regardless of who the winner is or which party won. I will only change this view if a seismic shift in view calls it in question. See “The Stock Trader’s Almanac” chart on election years from 1950-2022.

Source: The Stock Traders Almanac: 2024

In closing, we still live in interesting times and boring does not seem to be anywhere on the horizon. How that translates into the markets in the future is part of the adventure. The moves over the last few days have brought out all the bears and recession callers. It is simply too soon to declare this as anything but a garden variety correction in a seasonally appropriate time.

I continue to try my best for all my clients and help them meet their ongoing goals with levels of risk and reward that align with them. I look forward to our future conversations and meetings!

--JasonRASP Wealth Solutions, LLC is an SEC registered investment adviser. SEC registration does not constitute an endorsement of RASP Wealth Solutions, LLC by the SEC nor does it indicate that RASP Wealth Solutions, LLC has attained a particular level of skill or ability. This material prepared by RASP Wealth Solutions, LLC is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Advisory services are only offered to clients or prospective clients where RASP Wealth Solutions, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by RASP Wealth Solutions, LLC unless a client service agreement is in place. This material is not intended to serve as personalized tax and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. RASP Wealth Solutions, LLC is not an accounting firm. Please consult with your tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.